Adapt and thrive

How to turn a $310 negative cash flow property to a positive $2400 per month using this one strategy

How to turn a negative cash flow property to a positive cash flow in the midst of a rising rates environment ? Has your mortgage

Adapt and thrive

Adapt and Thrive Tips: What is the trigger rate and how to manage it?

https://www.youtube.com/watch?v=31uHeIo5eGA If you are in a variable rate mortgage product today where the payment has been fixed and stable during the rising rate environment that

Adapt and thrive

Quick tip: Some context please

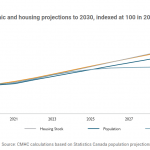

While prices may soften in the short term keep these important points in mind: We still need plenty of immigration to keep the economy strong

Adapt and thrive

Long term Perspective

With interest rates on the rise since early 2022, we have noticed an increasing level of fear, doubt, worry, and concern in the marketplace. Unfortunately

Adapt and thrive

BoC rate hike was extreme, however DON’T PANIC, we have a few suggestions!

I am sure you have all heard of the BoC announcement today!… No one saw those extra 25 basis points coming, but of course, it’s